Phwoar, look at the state of that. Camper van loaded up with surfboards (or are they paddleboards?!). I fantasise about the day I can switch off my laptop at my desk-job and wander the paths of Britain, cycle the roads of Europe and eat my way around the world.

However, I’m a cautious sort and the thought of just packing in my secure income keeps me firmly chained to the desk until an alternative springs out of the ground and slaps me in the face.

Now, I’m also quite a pragmatic sort, so am always on the look out for a way to get to that utopia of surfboard van-ing rather than dropping it into my “dream” drawer and buying a lottery ticket with fingers and toes crossed.

Previously, I thought the way to get there was go all-in on career, climb the ladder and earn that sweet $$ as quickly as you can before jumping ship a millionaire.

However, a high income doesn’t neccessarily equal high wealth (although with the right knowledge it makes it a damn sight easier). And for a cautious one like myself I need the security of wealth to act as a safety net. This wealth is “financial independence”.

Financial independence is defined as the point at which your living expenses are all met by passive, unearned income (as opposed to active, earned income such as paid employment).

Typically, you build up a portfolio to the value of 25x your annual expenses by investing into a low cost index fund.

Once you hit that magic number, you can then start withdrawing at a safe withdrawal rate of 4%. People often have different rates but this is the general rule of thumb (I’ll do a separate post about financial independence more generally, but today is about why I’m chasing it, sorry for being decadent)

You live off of that money, and your portfolio can continue to maintain / grow and so can support you indefinitely.

Boom, time for me to go on a perma-walk around Britain like a wandering vagabond!

The freedom, the flexibility, the security, and the time. It seems that financial independence literally provides the best of all worlds.

I’m not fussed about living in a massive house and always having the latest tech, I value experiences such as trudging across long distance paths and cycling over European flatlands in search of a Belgian beer (weird, I know!) and these things don’t need money more than they need time.

Free from the shackles of trading time for money, I won’t be so fussed about the potential financial returns of my projects and interests, which opens up a world of untapped potential!

I’m sure that you don’t need me to explain why the concept of financial independence seems such a worthy goal.

My journey to this point

After starting university in London, one of the most expensive cities in the world, I started to educate myself on personal finance so I could get a handle on my finances after being faced with the prospect of having to drop out due to no funds (I worked at a Vodafone store 20-30 hours a week in my 2nd year after rinsing through my savings in 3 months of first year!).

Once I escaped from the weeds of money mismanagement and the dust had settled around me, I started to re-assess some of my long-held beliefs about money.

I soon realised that a high income doesn’t necessarily equal large wealth, and that wealth is the true key to being “rich”, because it can provide a secure income stream all on its own.

I was headfirst into the world of consumerism at that point, with burning ambitions to be earning megabucks and drive a sports car wearing fancy clothes so everyone knew it.

Readjusting my ambitions to align with my new understanding that maintaining a strong savings rate was the bedrock to strong finances (a lifestyle which involves a much more frugal way of life) was a pretty painful process to say the least. Nowadays, I am not uber-frugal, as my income allows me to achieve a decent savings rate whilst enjoying a decent lifestyle.

I’m still a recovering consumerholic, and I still sometimes get caught out finding myself fighting the urge to buy some shiny brand or the latest tech. But for the most part, I’ve now been able to manage these urges (I’ll be sharing some of these techniques in a separate post) and can consistently hit a savings rate of 40%+, putting me well on my way.

Don’t get me wrong, if I continue to boost my income and invest aggressively with my personal profit, I may still allow myself a fancy sports car if the income from my portfolio allows it.

2021 update: read how I saved for a house deposit in 12 months

So how does a high income not necessarily equal high wealth?

Savings rates and habits.

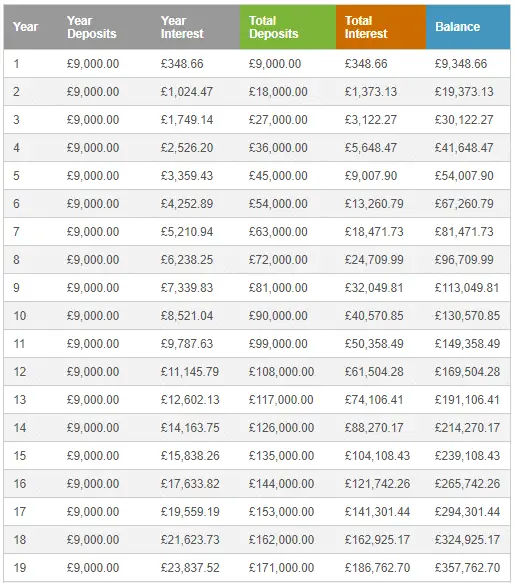

Imagine Bill is 25 and earns £30k a year (so his after-tax income is £24k per year, around £2k per month) but only spends £14k on his living costs. He drip-feeds that left-over £9k a year into a well-diversified, low-cost index fund which averages a 7% real annual return (i.e even taking into account inflation). He still lives well on his £14k a year, but he knows that investing his left-over money of £750 will be worth it.

In order to retire, Bill needs passive income of £14k per year to cover his expenses. Assuming he hasn’t got any online businesses which prop up that income and he doesn’t want to do any active work at all, he will need a portfolio of roughly £350k to support him (we will touch more on this in a separate post, but a general rule of thumb is 25 x your annual expenses).

Bill receives subsequent payrises, and is happy with the rate at which he is saving so he uses all of his extra money to pay for nice new holidays and the occasional fancy restaurant meal.

He is able to reach his target figure of £350k at age 44 and is able to retire. Not bad for someone who hasn’t won the lottery, become the CEO of a FTSE 100 firm or been able to have a successful exit from a new tech firm.

What is more, his money is now working for him. His portfolio is generating him returns of ~£24k per year (assuming 7% average annual return). Remember when he was working 35 hours a week and getting paid £24k after tax? Now his money is doing the earning for him.

Compare this to Jack. He is 25 and earns £50k a year, but he spends almost all of his earnings on the good life. He’s got a nice flat in the middle of the city, drives a brand new BMW on lease, has the newest iPhone and a fancy watch.

It’s a great lifestyle and everyone thinks Jack is doing really well (as he’s sure to tell everyone at every opportunity). As he goes further through his career, Jack’s salary continues to increase and he continues to increase his spending. He’s now 44 and doesn’t have any savings to speak of, and has to continue working to fund his lavish lifestyle. It is now a cycle that he is essentially trapped in until he can retire at the normal pension age.

Now once again, this is a personal viewpoint. That second example may be an ideal fit for some of you reading this. You get to enjoy your lavish lifestyle, and you retire like everyone else when you get to retirement age (chances are with that job, you’ll also have a decent retirement pot too to continue a reasonably luxurious lifestyle).

However, what appeals to me so much about the first example is the flexibility and freedom. Bill could retire much sooner than 44 if he re-invested his pay-rises, boosted his income via other channels and kept a lid on his spending.

In the first example (Bill), you have your freedom more than 20 years earlier than the standard route. This freedom provides you the financial security (you can absorb any unexpected losses in earned income, any unexpected events etc), but critically it also provides you with time that can be used elsewhere.

Of course, this timeline could be sped up if Bill was willing to go all-in.

At 44, Bill may decide to continue working, but part-time. He may decide to do some charity work for a cause he is passionate about. He may re-train and chase a path he has always wanted to do but felt constrained by financial pressures.

Remember as well that the Bill example is not that unachievable. He didn’t require an extremely high salary (although granted the example used an above average salary for the UK). He didn’t require in-depth knowledge of investing and financial markets to get the return of 7% per year either, we will cover all of this.

What it did require is discipline, knowledge and consistency.

Additionally, if you’re able to grow your earnings more aggressively (either from your job or from side businesses), you will be able to achieve FI quicker. The internet has loads of examples of people who were able to achieve independence on an aggressive timescale.

Emma App Review: Is It the Best Spend Tracker Out There?

A key part of managing your personal finances is tracking your spending. You can use…

Should I Save an Emergency Fund or Pay Off Debt?

Maybe you’ve been gifted some cash or come across a windfall. Or you’ve engineered yourself…

How to create a personal budget in Excel that’ll even impress your accountant!

When creating a budget, using a spreadsheet app like Excel makes the whole job much,…

Why starting to save when you’re young is so important (I wish I did more of it!)

I’m sure most people are in the same camp as me, but I regret not…

How to cancel The Economist subscription and stop it from auto-renewing

I always harp on about giving your finances a shot in the arm by cutting…

How To Cancel NFL Game Pass UK

Looking to trim back your subscriptions? Good on ya! In this article, we’ve pulled out…

Moneyfarm vs Vanguard: Lowest Fees On The Market?

Investing is the most impactful tool you have to reach an ambitious financial goal. Sometimes…

Moneyfarm vs Nutmeg – The Battle of the Robo Advisors

Looking to invest to reach your financial goals? Fortunately investing nowadays is much more accessible…

Yolt Review UK 2021 – Does This Take The Throne?

If you’re looking to get on top of your finances, an app can do some…

Snoop vs Money Dashboard

An app has the power to simplify your life. Especially your finances. Rather than cracking…