I’m sure most people are in the same camp as me, but I regret not starting to save more when I was younger.

I would manage to be disciplined and save up some money, £500 or so, and then have one big blow out and buy a laptop or something else I probably didn’t need.

Then I’d start from scratch and the cycle would repeat itself.

You’re obviously smarter than I am, and are here to educate yourself on how you can set yourself up for some big financial goals, which starting young helps to give you a foot up on.

Even if you’re not all that young, today is the best time to start!

There’s an old Chinese proverb which hits the nail on the head when it comes to investing;

- Why starting to save when you’re young has a massive impact on your wealth

- What is compounding?

- What does compounding need to work?

- £60k doesn’t inspire me, give me some bigger numbers

- But hang on… I don’t want to wait until I’m 70!

- The FIRE formula

- Bob wants to retire early

- Quick tips to help you save when you’re young

Why starting to save when you’re young has a massive impact on your wealth

It will get you into good habits

If you’re used to saving from a young age, you’ll have instilled some good habits that will stand you in good stead when your responsibilities, income and temptations increase.

It will give you options

Having some cash in the bank at a young age will give you options a lot of your peers won’t have (unless they’re funded by the Bank of Mum and Dad).

You’ll have the flexibility to experiment and go travelling, or to invest in yourself with specialist training courses, or heck even to re-train if you don’t like the route you found yourself on.

You have time on your side

Even though you may not have much experience on your side, you have an abundance of the most precious resource; time.

It is simple why starting to save when you’re young has such an impact on your ability to grow wealthy:

Compunded returns.

If you save and then invest this, it will give you the ability to set a tangible path to your financial goals that will leave your peers dripping with envy.

What is compounding?

Compound returns are when you earn a return on your investment, which then goes on to earn a return itself.

A simple example is with a simple interest-paying savings account.

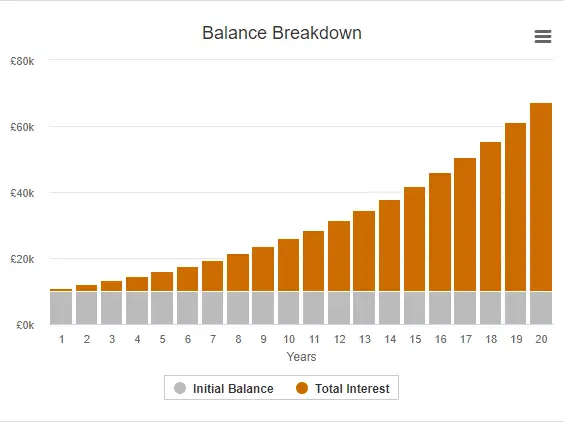

Imagine that Bob has put £10,000 into a savings account that pays him a 10% interest rate (theoretically, as there is NO chance ol’ Bob is getting an account paying that interest in the current climate).

In Year 1, Bob earns £1,000 which is 10% of £10,000. He now has a balance of £11,000.

This £11,000 is now earning interest of 10%, rather than just his original £10,000.

In Year 2, Bob earns £1,100 which is 10% of £11,000. He now has a balance of £12,100.

If this were to continue for 20 years, Bob would have a balance of just over £67,000. All whilst only paying in his initial £10,000.

In the graph below, you can see the grey portion of the bars remain flat because Bob has not paid in anything more than his initial £10,000.

Over time, you can see it slowly builds and builds, but as more interest is earning interest which is earning interest, the amount he earns in interest each year (and re-investing) increase dramatically.

In year 1, he earned (and re-invested) £1,000.

In year 20, he earned just over £6,000!

Of course, this example uses a fictitious 10% savings rate example – but it is purely to illustrate the concept.

In reality, leaving your money in a savings account is rarely the best option (unless building up an emergency fund or saving for a short-term financial goal). The better option is to invest.

The main investments are:

- Stocks and shares (owning a piece of a company)

- Individual shares

- Funds (active or passive)

- Bonds (essentially lending money to companies or organisations, who pay you an interest rate)

- Property

- Either directly, such as buying a house to let out

- Or through a fund on the stock market

What does compounding need to work?

Time, patience and re-investment.

With each piece of interest and return you receive, you should re-invest it. If Bob spent each year’s interest then he would be left with a balance of £10,000 in 20 years time, compared to the balance of over £67,000 with his returns re-invested.

Once re-invested, you need to simply be patient and let time take its course.

£60k doesn’t inspire me, give me some bigger numbers

Sure. Let’s make him a millionaire.

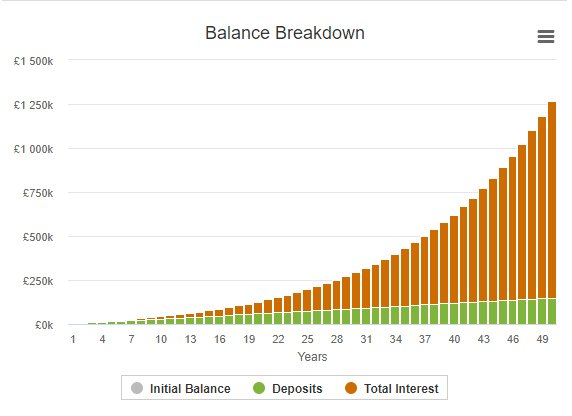

Let’s say that Bob didn’t have £10,000 to invest, but instead engineered himself a personal profit of £250 by being smart with his money and living frugally where he can.

He’s only 20 when he starts, and he invests this £250 a month in the stock market via a diversified fund, earning a 7% annual return.

As a side note on investment returns:

It is possible for him to earn a return higher than 7% on average, with the FTSE100 earning an average annualised 7.8% return between 1984 and 2019 (the FTSE 100 is a tracker looking at the largest publicly listed companies in the UK), with 2019 generating a return of 17.1% in that year alone!

Bob is patient and diligent and is able to continue putting in £250 a month without taking any out, whilst also re-investing any dividends he might receive.

Why should you re-invest your dividends? Because it makes up a part of your investment’s return. And the more you keep invested the more your “interest” is earning “interest” as more is kept in earning a return of its own.

If he sticks with it, then Bob will retire with over £1.2m!

He would have only paid in a total of £150,000 over 50 years, earning over £1.1m from his returns over the period.

In 50 years’ time, when Bob is 70, his portfolio is earning him returns of nearly £83k per year!

But hang on… I don’t want to wait until I’m 70!

Bet you don’t. I sure as hell don’t want to!

If you are able to increase your monthly investment (by earning more or spending less), then you will accelerate this process.

Or alternatively (/additionally) if you’re able to achieve higher returns than the stock market average then this will be accelerated.

However, another route that will accelerate your route to early retirement is planning your exit.

The FIRE formula

In the FIRE movement (financial independence, retire early), financial independence is touted as the goal which is defined as the point when your investment portfolio can support your expenses.

This means that your goal, your portfolio size, is dependent on your annual expenses.

If you bring down your expenses (and can sustain happily at that level), then you need a smaller portfolio.

To calculate the size of portfolio you need, multiply your annual expenses by 25.

This is based on the rule of thumb that you can take out 4% of your portfolio annually to pay for your living expenses, with your fund not depleting in size over time – essentially being able to support you indefinitely.

So if you have annual living expenses of only £10,000, you only need a portfolio of £250,000.

If you have annual living expenses of £15,000, you need a portfolio of £375,000.

If these go up to £20,000, you need £500,000.

You get the idea!

Bob wants to retire early

Now, if Bob has annual expenses of £15,000 and is happy with his lifestyle at that level and considers it to be sustainable, he needs a portfolio of £375,000 in order to sack off his day job and retire early.

If he was able to sock away £250 a month from the age of 20, he would be able to retire in his early 50s, before his 54th birthday. This is over 10 years earlier than people normally retire, and all for £250 a month (calculations here).

If he was able to increase his monthly deposits by 5% each year, he will be able to retire in his late 40s, not long after his 46th birthday (calculations here).

If he was able to invest even more, then this would happen even sooner.

Quick tips to help you save when you’re young

The more savings you can put away each month, the more you can invest.

Set a budget

Even though this will probably fill you with dread (and boredom!), I promise you that setting a budget will be a very impactful exercise for your finances.

Grab a list of your income and expenses to work out what you typically spend/earn, and then work through and try to cut your expenses for a quick shot in the arm for your budget.

Try to experiment with methods of sticking to your budget

It took me AGES to find a method that works.

My method is simple. I allocate out my money each time I get paid so my money has a “home”. I put the budget for my discretionary spending (the kind of money that I budget for going out for drinks, playing sports etc) into a separate current account with which the card is the only one I carry around (so I can’t get tempted by putting stuff on my credit card).

Travel cheaply

Relish the ability to travel on the cheap by taking the train through countries and staying in hostels – you won’t want to do it forever so its a great way to see the world on a tight budget that actually enhances your experience.

Be mindful with your spending

Just because your friends are buying the latest iPhone or have flashy clothes, doesn’t mean you need to.

Find a balance that works for you, but know that working towards your financial future is never a bad thing. If you’re busy working towards a secure, happy and bountiful financial future, they’ll likely be spinning their wheels with zero wealth and zero options but to continue working.

Get a job!

It doesn’t matter what, but getting a job (including in your summers or to supplement your income at university) will give your finances a massive shot in the arm.

I was only able to stay in university because I got a part-time job, but I was able to get some valuable experience, meet some new people and add another string to my CV that set me up well for my post-university job.

Understand opportunity cost

Opportunity cost is the trade off you make when you make a decision (the benefit you would have received if you had gone for a different option).

For example, the opportunity cost of spending £10,000 on travelling is the lost interest of putting it into savings (or the lost return you could have made if you had invested it).

Life is full of trade-offs, and it will help you to be intentional and mindful with your spending when you consider these.

Continue to educate yourself

Just because you’ve left school doesn’t mean you stop educating yourself.

The fact that you’re here shows that you are keen to further your knowledge, and I applaud you! Keep on going and stick with it and you’ll reach your goal.

How To Cancel Glossybox UK

Wanting to cancel your monthly beauty box subscription? We’ve laid out the steps you need…

How to cancel The Gym membership

Sick of the gym or found a better option? Nice. Most gyms are an absolute…

Average Cost of Food For One Person UK

When looking at your own food costs, it is often difficult to know how you’re…

Does PayPal Credit Affect Credit Score?

Even though consumer credit, in general, has shrunk in the UK since the start of…

How To Cancel Gousto Subscription UK

Bored of the recipes or wanting to try a different provider and looking for instructions…

Pain-free vs Painful Savings

As part of the Budgeting 101 article, I discussed the lengths you’ll need to go…

How to create a personal budget in Excel that’ll even impress your accountant!

When creating a budget, using a spreadsheet app like Excel makes the whole job much,…

How to Save Money Using Envelopes

As we come up to the new year, lots of us will be setting new…

17 Actionable Tips on How to Pay Off Debt Faster

You’re not alone. Living with debt has become a common issue for people in the…

How To Cancel Graze Subscription UK

Bored of your Graze boxes or want to try a competitor’s version? We get you….

Pingback: How to control impulse spending - 8 strategies that work - Personal Profit

Pingback: Average net worth in the UK - how do you compare? - Personal Profit

Pingback: Is Saving £1000 a Month Good? | The Mindful Money Project

Pingback: What should I do with spare cash? | The Mindful Money Project

Pingback: What is the difference between income and wealth?