A profit and loss statement is how a company keeps track of all of its income and all of its expenses. It allows the management and owners to understand whether it is making money, a profit, or whether it is losing money, a loss.

A personal profit is the same concept, applied to a person’s financial situation (rather than that of a company).

It is quite easily described as all of your income less all of your expenses in a certain time period to arrive at your profit figure. In personal finance terms, people normally refer to this as your savings rate.

So if you receive £2,000 per month after-tax, and you spend £1,500 per month, your personal profit is £500 per month. This is a savings rate of 25%. In the business world, this would be your profit margin.

Personal profit can be expressed formulaically as;

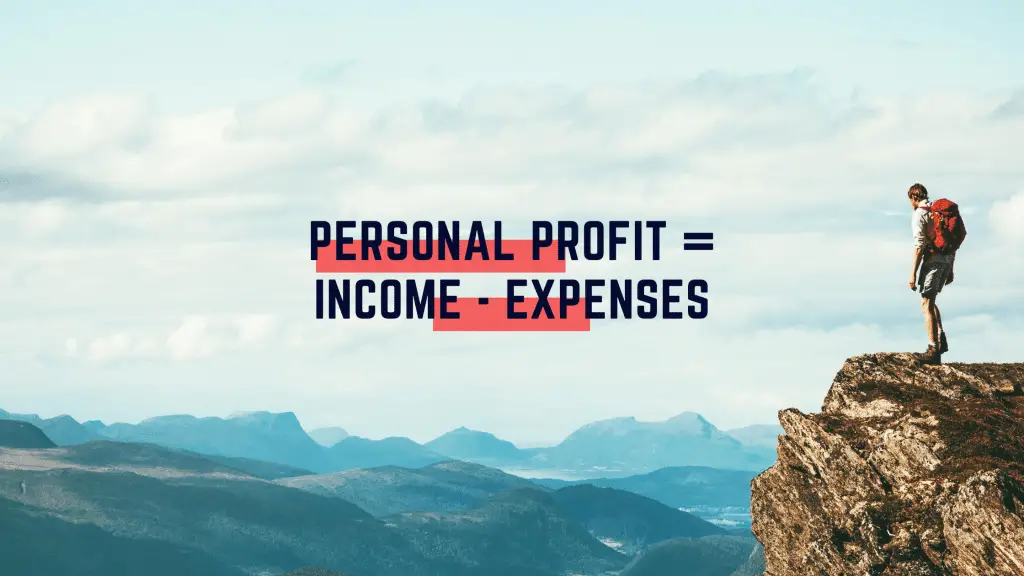

Personal Profit = Income – Expenses

Why is it important?

You may be a devout follower of the ostrich school of personal finance, where students are encouraged to firmly place their head deep within the sand.

However, this can be dangerous if you find yourself in a situation of worsening finances. If you can name any of the below symptoms, then you need to start looking at your finances in more detail to understand what is going wrong, and finding the areas to fix it:

- Are you itching for next payday because you always seem to run out of money before the month is up?

- Are your credit card balances increasing each year?

- You put money away in a savings account but always have to draw back on it before each month finishes?

The cause is likely the same; your expenses are higher than your income on average and you are therefore making a personal loss. If you were a business, you’ll run out of money at some point and go out of business.

For a personal finance situation, you want to avoid being in a loss for too long. Doing so means at best your savings are eroded and at its worst it could send you into a debt spiral. A debit spiral is when you need to take on consumer debt to pay for your lifestyle, which grows larger when you add in the additional interest costs of the debt, which then requires you to take out more consumer debt to service the initial debt, which then adds on even more interest costs etc etc.

What side should I focus on first – expenses or income?

Most personal finance blogs only focus on one side of the equation; expenses. They focus on the best methods for saving and budgeting, but they ignore the income side altogether.

You should definitely first start with putting in place a budget. This will help you understand your current spending level and compares that with your income to arrive at your current personal profit statement.

It gets a hard-rap, but your budget will be the most important tool in bringing your expenses down to a more reasonable limit in line with your income, by identifying areas for saving.

Making savings, especially pain-free ones, tend to be the quickest way to give your personal finances a shot in the arm. Most of the time they are directly under your control, and can be implemented really quickly.

Making sure you eliminate any wasteful spending should be a priority even when you’re in a good financial position.

However, past a certain point making savings will become harder and harder as they will require more and more painful savings that need underlying lifestyle changes. Some of the time this will be beneficial, but there is always a floor to the savings you can make as you still need some to live.

Whereas the income side of the equation has limitless upside. In theory, you could earn billions.

If we keep the same example that I used earlier in the article, where you receive £2,000 per month after tax from your job, and your expenses are £1,500 per month, your current personal profit is £500 per month. However, if you increased your income by a further £500 per month, your personal profit has increased by 100% to £1,000 per month! That now means that you have a savings rate of 50% (up from 25%)!

Of course, having the intention to boost your income and actually succeeding in boosting your income are two different things.

I will go through many of the routes open to you as well as the ones I have had success with in a future article, but for now I encourage you to check out this wonderfully detailed article on matched betting for UK readers – a really powerful way to boost your income.

For the eagle eyed accountants out there, this view of personal profit for a persons finances is actually more like a cash flow statement, or a cash-based P&L. Unless you have more complex finances, it is unlikely investing the time into driving and maintaining an accruals-based P&L will be worth it in terms of the insight it provides.

Average Cost of Food For One Person UK

When looking at your own food costs, it is often difficult to know how you’re…

Average net worth in the UK – how do you compare?

Even though comparing yourself to others doesn’t always do your mental health much good, it…

How To Cancel Virgin Active Membership UK

Looking to trim back your subscriptions and cancel your Virgin Active membership in the UK?…

What Is A Good Amount Of Savings UK?

Generally in life, more tends to be better. But is that true for savings? Whilst…

How to cancel The Gym membership

Sick of the gym or found a better option? Nice. Most gyms are an absolute…

Is Saving £1000 a Month Good?

Saving £1000 a month is quite an iconic milestone for many of us. A big…

The Big Bad Budget – My Top 5 Reasons Why You Need A Budget

Budgeting. The word alone has probably sent shivers down your spine. It is a strangely…

Yolt vs Money Dashboard – Who Wins?

We have an app for everything nowadays. Using an app can remove the heavy lifting…

How To Cancel Virgin Wines Subscription UK

You’re a lover of wine but sick of the subscription, we get it! Are you…

Yolt vs Money Dashboard vs Emma – The Comparison!

Don’t want to dust off a spreadsheet? A budgeting app can do most of the…

Pingback: Uh Oh, What Even Is A Budget? - Personal Profit Builders

Pingback: How The Timeframe of Your Personal Finance Goal Makes A Big Difference - Personal Profit

Pingback: The Big Bad Budget - Top 5 Reasons Why You Need A Budget - Personal Profit

Pingback: How To Stick To Your Budget When Nothing Works - Personal Profit

Pingback: How I Paid Off £2,000 Debt and Saved £9,000 In Less Than One Year - Personal Profit

Pingback: How To Calculate Your Savings Rate - Savings Rate 101

Pingback: Average Food Budget in the UK - How Do You Compare? - Personal Profit

Pingback: How Big Should My Emergency Fund Be? - Personal Profit

Pingback: 7 tips in how to stop living paycheck to paycheck - Personal Profit

Pingback: How to create a budget in excel that'll even impress your accountant!

Pingback: Can saving money make you rich? - Personal Profit

Pingback: Why starting to save when you're young is so important

Pingback: How to deal with a financial emergency step by step: dealing with income loss - Personal Profit

Pingback: How to deal with an unexpected expense - Personal Profit

Pingback: Average net worth in the UK - how do you compare? - Personal Profit

Pingback: What is the difference between income and wealth?

Pingback: What are the benefits of budgeting? - Personal Profit

Pingback: What should I do with spare cash? - Personal Profit

Pingback: How to budget when you get paid weekly

Pingback: The 7 biggest finance mistakes young professionals make in their 20s

Pingback: Pain-free vs Painful Savings | The Mindful Money Project