With nearly 17% of jobs getting paid weekly, you’re certainly not alone in trying to fit budgeting advice, designed for people who are paid monthly, to your weekly-pay situation.

I must admit, I’m guilty of writing most of my budgeting tips with monthly-paycheckers in mind, but in this article, I’m going to set that straight and show you specifically how to budget when you’re paid weekly (if you get paid monthly – check out my other budgeting article here).

How getting paid weekly is actually an advantage

I always struggled to stick to my damn budget on spending for more discretionary items like groceries and entertainment.

I always get suckered into buying shiny stuff at the supermarket or agreeing to go out for more beers/food/burgers than my belly wallet can handle.

The best way I’ve learned to manage it is by transferring a weeks’ worth of my monthly travel/groceries/entertainment budget into a completely separate current account each Friday (which is the only debit card I carry around with me).

This means that when I’m out and about and faced with a spending choice, I simply flick up my banking app and check how much I have. It instantly provides me with an answer. I know that I’ve got £x amount left to last me until the next Friday’s hit of money.

By getting paid weekly, you don’t need to engineer this drip-feeding into your account and instead you have it built-in by default. In the immortal words of Borat; great success!

D’oh – how getting paid weekly adds some complexities

On the flip side, monthly, quarterly or annual expenses are a bit of a nightmare to build up to. Whereas with a monthly paycheck you can pay the full months’ rent/mortgage payment straight away, it isn’t that simple with a weekly paycheck.

This is where building up to the full months’ bill is important and why you need to put this aside from each week’s paycheck to make sure you can pay your important expenses.

The other area that becomes harder with a weekly paycheck is cash flow. The timing of your bills out of your account matter. In an ideal world, all of your big bills may come out at the end of the month where you have 4 weeks to build up to them, but in the real world it is rarely that simple.

These are all complexities that I will help you navigate.

Set up the foundations; a monthly budget!

“Eh, your article on how to budget when you’re paid weekly is starting with a monthly budget? Get lost Greg!!”

Trust me, the monthly budget will become the bedrock of your finances regardless of how often you get paid, which we can then adapt to your weekly paycheck.

To arrive at your monthly budget;

- Tag up transactions of your last 6-12 months’ worth of bank statements identifying income and expenses (the main expense categories I use are Groceries, Entertainment, Travel, Holiday, Housing and Bills, but you can go more detailed if you like).

- Find out your average monthly spend by taking the total of each category and dividing by the number of months’ worth of data you have (i.e if your total for Travel is £1,000 and this is over a 6 month period, your average travel spend per month is £1,000 / 6 = £167).

- Set a monthly budget for each of these categories which ensures you are making a personal profit. A personal profit is where your income is higher than your expenses. Make use of your average historic monthly spend to figure out areas where you may struggle to meet the budget. Make sure that you have included any non-regular spend that may happen once or twice a year for example Christmas or Holidays. For any areas that your budget is far from your average historic spend;

- Make savings if your expenses are higher than your income until you are in the position of making a personal profit in your budget. Do this by making savings, adjusting your budget and checking to see if you are making a personal profit after each iteration. For example, if your entertainment line is too high each month compared to your budget, run through the transactions and cut back on some regular expenses to make sure you’re able to hit your budget.

The aim of having a budget is for it to be;

- realistic and achievable (by being rooted in historic spending and any planned or achieved savings)

- makes you take action (such as identifying areas for saving)

- gives you accountability (you have an explicit target that you want to track against)

- helps you forecast for the future (you know that if you hit your budget each month you have £x per month that you can save/pay off debt with, allowing you to figure out how long it will take to reach your financial goals).

It needs to be in a position where you are making a personal profit. This is where your income is higher than your expenses.

If you are not in this position, then continue to find areas to save money (or boost income) until you are in a position of making a personal profit.

Good areas to look for savings are:

- Subscriptions (Netflix, Amazon Prime etc)

- Mobile phone bills

- Utility bills (try a comparison site to check for a cheaper deal)

- Swapping to cheaper/free alternatives (swapping Sky for Freeview as an example)

- Grocery shopping (how do you compare to the UK national average weekly food budget?)

Identify the important payments that need to be made monthly

Your important payments are the ones that you need to hit, otherwise bad things will happen!

Typically these will be:

- Housing (rent/mortgage)

- Utility bills (water/gas/electricity etc)

- Other bills (telephone, broadband, TV, TV license, mobile phone)

- Credit card/loan repayments

Mark out whether they are due weekly, monthly, quarterly or yearly so you can understand how often your payments go out of the bank, along with the due date (i.e if you pay your monthly rent payment on the 1st of each month).

This will help you to build a view of your ins and outs and will help you to spot any cashflow issues upfront. If it helps, grab hold of a physical calendar and a big marker pen and write out the ins and outs on this to make it really visual.

Adapting your monthly budget to a weekly paycheck

Calculate your weekly budget

Once you have your monthly budget as per the above, you can easily adapt it to weekly to understand the amount of money you need to put away and where in order to pay your bills.

To adapt your monthly budget to weekly, take your monthly budget and divide by 4 weeks.

Let’s use an example to demonstrate this, with good ol’ trusty William the weekly-paid wordsmith. William gets paid £500 per week after-tax, and has figured out his monthly budget is £1,500 (he’s a fairly frugal chap to be fair to him!).

From this, we can work out his weekly budget is £375 (£1,500 / 4).

His weekly income is £500, and his weekly budget is £375. The remainder, £125 (£500 – £375) is his “personal profit” and is his to use to save, pay off debt or invest.

But that is underestimating the number of weeks in a year!

The eagle-eyed among you would have spotted that doing this actually underestimates the number of weeks in a year. We know there are 52 weeks in a year, but this method assumes there is only 48 (4 x 12) and is therefore overstating your budget.

The reason I recommend dividing your monthly budget 4 weeks is that every month has at least 4 paydays in.

This means that in a world where your largest bills are going to be monthly payments (think rent / mortgage, council tax, car insurance, electricity, gas etc), you want to have a full months’ worth of money saved up to pay it even in months where you only have 4 paydays as opposed to 5.

If we went the more scientific route of working out the exact weekly budget by doing your monthly budget multiplied by 12 months, divided by 52 weeks of the year then you will find that in some months you don’t have a full month worth of rent/mortgage payments whereas in others you will have too much.

Of course, this averages out over the year, which is why it works mathematically, but is not helpful for you when you’re short on rent in certain months!

If you follow this each week for a full year, you will find that you have an automatic buffer building up in your budget. In the example of William the wordsmith above, he will have a buffer of £1,500 at the end of the year if he hit his budget – not bad!

Allocate your money each payday

When you get paid each week, you want to be allocating your money out into separate “pots” ready to be used at different times.

This allows your housing costs and bills (your important items you identified above) to be taken care of, by building them up over the full month ready for them to be taken out when paid monthly.

This is a version of the piggybank/envelope method which is also the technique I use to stick to my budget on autopilot and with minimal effort.

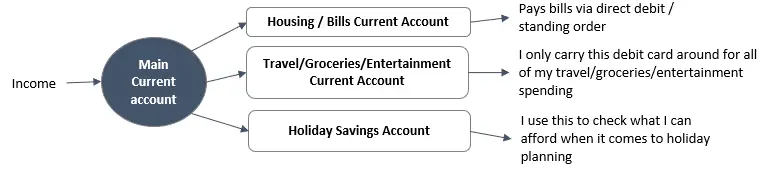

My setup is below, which would work just as well if I was being paid weekly, which allows me to transfer my housing/utilities budget into a completely separate housing/bills account which has standing orders and direct debits set up.

I know that once I fund this account, my housing costs and bills are all taken care of and I have nothing else to worry about.

I also transfer my travel/groceries/entertainment budget into a separate current account. This is the only card that I carry around with me on a day to day basis to stop me from being tempted to splurge on my credit card.

How to deal with timing issues on monthly payments

Move payment dates

Ideally, you want a 4-week run-up to hit your monthly bills, so moving all of your monthly bills to the end of the month may provide you with this, as well as simplifying your financials by having all of your monthly bills come out around the same time.

The risk to this approach is that if you have not been able to save your weekly budgeted amounts to build it up over the month, you will be hit all in one go.

However, if you follow the process above of allocating your weekly budget into a separate account, then you should have this money saved up by the time the bills come rolling around.

If you are unable to move your payment dates or don’t want to, then you have another option.

Build up a buffer

If you have an emergency fund, I would put some of it into your housing/bills account to provide you with a buffer against timing. Be sure to replenish your emergency fund with your personal profit as soon as you can.

Having this buffer in your account will mean that you can ride out any timing issues on when your bills are due.

The amount will vary from person to person, but try to build up a buffer of 1 months’ rent/mortgage. This will mean that you can pay this whenever (the most important expense!) and then your weekly budget allocation will bring you back up.

Hopefully, this article helped you if you get paid weekly. Do you have any techniques and methods you use that allow you to budget on a weekly paycheck? Drop a comment in the comment section below.

Easy and painless ways to save money every month

Maybe you’re preparing for a particularly financially tight month. Or you’re looking for ways to…

3 of the Best Budgeting Apps for Young Adults in the UK

As a young adult with a wealth of opportunity ahead of you, I salute you…

Yolt vs Cleo: Will One of These Help Your Finances?

Another budgeting app face-off. This time, we pitch Yolt vs Cleo. Quick Summary For those…

Best Budgeting Apps for Families

Staying on top of your own finances is a difficult enough task, yet add a…

Are Money Saving Apps Safe?

Ah apps. Love them or hate them, they are an increasingly important part of our…

How to set up a budget in Google Sheets

The trusty spreadsheet is no longer dominated by Microsoft Excel. Google’s offering; Google Sheets, is…

How To Cancel Virgin Active Membership UK

Looking to trim back your subscriptions and cancel your Virgin Active membership in the UK?…

How to deal with an unexpected expense

This always seems to be the way of the world – you’ve managed to get…

How To Cancel eHarmony UK

Looking to cancel your eHarmony account in the UK in a few easy steps? Look…

Money Dashboard Review UK 2021 – Will This Sort Out Your Finances?

If you’re not interested in tracking your spending using a spreadsheet, then using a budgeting…